All Categories

Featured

Table of Contents

Just choose any kind of form of level-premium, long-term life insurance plan from Bankers Life, and we'll convert your policy without calling for proof of insurability. Policies are exchangeable to age 70 or for 5 years, whichever comes later on - term life insurance for married couples. Bankers Life offers a conversion credit scores(term conversion allocation )to insurance holders up to age 60 and via the 61st month that the ReliaTerm plan has actually been in pressure

At Bankers Life, that means taking a customized technique to aid secure the individuals and family members we offer - what is extended term life insurance. Our objective is to give exceptional solution to every insurance policy holder and make your life less complicated when it comes to your cases.

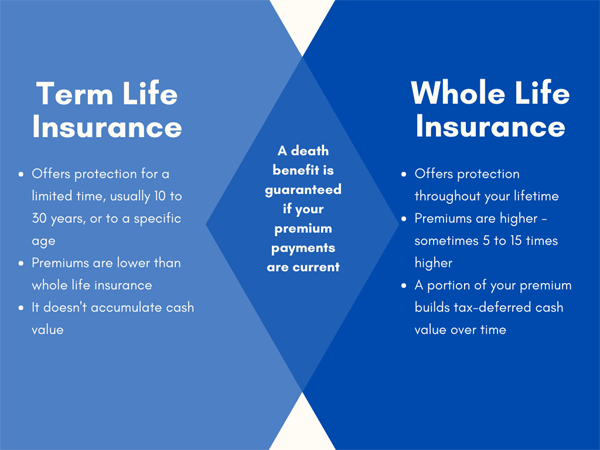

Life insurance providers provide numerous forms of term plans and standard life plans as well as "interest sensitive"items which have become extra widespread considering that the 1980's. An economatic whole life policy supplies for a fundamental quantity of participating entire life insurance with an extra extra insurance coverage given with the usage of rewards. There are 4 standard interest sensitive whole life plans: The global life policy is actually more than interest sensitive as it is made to show the insurer's existing death and expense as well as interest earnings instead than historical prices.

You might be asked to make added costs repayments where insurance coverage can end due to the fact that the rate of interest dropped. Your starting interest price is repaired just for a year or in many cases 3 to five years. The guaranteed price offered in the policy is much lower (e.g., 4%). One more feature that is sometimes stressed is the "no price" car loan.

Best Decreasing Term Life Insurance

In either situation you should receive a certification of insurance coverage defining the stipulations of the team plan and any type of insurance policy charge. Typically the maximum quantity of coverage is $220,000 for a home loan and $55,000 for all various other financial debts. Credit history life insurance policy need not be bought from the organization giving the finance

If life insurance is called for by a creditor as a condition for making a lending, you might be able to assign an existing life insurance policy, if you have one. Nonetheless, you might desire to purchase group debt life insurance policy in spite of its greater price due to the fact that of its benefit and its availability, typically without in-depth proof of insurability.

However, home collections are not made and costs are sent by mail by you to the agent or to the company. There are certain aspects that tend to raise the costs of debit insurance policy more than routine life insurance policy strategies: Particular expenditures are the very same regardless of what the size of the plan, to ensure that smaller policies issued as debit insurance will certainly have higher premiums per $1,000 of insurance policy than bigger dimension routine insurance policies

Because early lapses are pricey to a company, the costs have to be handed down to all debit insurance policy holders. Given that debit insurance is created to include home collections, greater payments and fees are paid on debit insurance policy than on routine insurance coverage. In most cases these greater expenses are passed on to the insurance policy holder.

Where a company has various premiums for debit and routine insurance it might be possible for you to acquire a bigger quantity of regular insurance policy than debit at no added price - when looking at a rate table for supplemental term life insurance, what are the rates based on?. Therefore, if you are thinking about debit insurance coverage, you should absolutely check out normal life insurance coverage as a cost-saving option.

The Combination Of Whole Life And Blank Term Insurance Is Referred To As A Family Income Policy

This plan is made for those who can not originally manage the normal entire life premium yet who desire the higher costs coverage and feel they will become able to pay the higher costs (a long term care rider in a life insurance policy pays a daily benefit). The family policy is a mix plan that gives insurance security under one agreement to all members of your instant family other half, other half and youngsters

Joint Life and Survivor Insurance provides coverage for 2 or more persons with the survivor benefit payable at the death of the last of the insureds. Premiums are dramatically lower under joint life and survivor insurance than for plans that insure just one person, considering that the possibility of needing to pay a death case is reduced.

Costs are dramatically more than for policies that insure a single person, since the chance of having to pay a death claim is greater (maryland term life insurance). Endowment insurance coverage offers the payment of the face total up to your beneficiary if death occurs within a details amount of time such as twenty years, or, if at the end of the certain period you are still alive, for the repayment of the face total up to you

){kind=link}

Latest Posts

What Is A Direct Term Life Insurance Policy

Term Life Insurance For Police Officers

Term Life Insurance For Pilots